Food Costing

15 The Principles of Menu Engineering

Although you likely have a target overall food cost in your establishment, not every menu item will carry exactly the same food cost percentage. Some items are more costly than others, but most establishments will have a range of prices that all the menu items fit into. Consequently, it is important to balance the menu so that the low and high food cost items work together to help you reach your target food cost. This process is called menu engineering. Menu engineering means balancing the high and low food cost items; it also includes strategically featuring or promoting items to help reach your targets.

Calculating Menu Item Costs

The cost per portion derived from yield tests done on the main ingredient of a menu item usually represents the greatest part of the cost of preparing the item (see the section above on yield tests for more information).

However, of equal importance is the portion cost factor. For example, the portion cost factor can be used to determine the cost of a portion of the main ingredient regardless of the price of the meat (which is often the main cost factor) charged by the supplier as long as the restaurant’s preparation of the meat remains unchanged. The cost per portion is determined by multiplying the portion cost factor by the packing house’s price per kilogram (or pound).

Quite often the cost per portion of the main ingredient is used by itself to determine the selling price of a menu item. This works well with items on an à la carte menu as the basic main ingredient (such as a steak) is sold by itself and traditional add-ons (such as a baked potato and other vegetables) are sold separately.

As discussed earlier in this book, in many cases, some of the components will be the same, so a basic plate cost can be used to add to the cost of the main protein to get a total cost for the dish.

In dishes where the main ingredients are not sold as entities but as part of a prepared dish, the cost of all the items in the recipe must be determined to find an accurate portion cost price. In this case, a recipe detail and cost sheet is used to determine the cost price of menu items. (Refer back to the section on costing individual menu items for more information.)

Once the potential cost of a menu item is determined, the selling price of the item can also be calculated by using the food cost percentage.

Food Cost Percentages

As you may recall, food cost percentage is determined by dividing the portion cost by the selling price:

Example 30: Food cost percentages

food cost percentage = portion cost ÷ selling price

If the portion cost is $4.80 and the selling price is $14.00, the food cost percentage is:

food cost percentage = portion cost ÷ selling price

= $4.80 ÷ $14.00

= 0.34285

= 34.285%

= 34% (rounded off)

Another way of expressing the food cost is as a cost mark-up.

Example 31: Cost mark-up

The cost mark-up is determined by reversing the food cost percentage equation:

cost mark-up = selling price ÷ portion cost

The cost mark-up can also be determined by dividing the food cost percentage into 1. The equation then becomes:

cost mark-up = 1 ÷ food cost percentage

In the example above, where the portion cost is $1.20 and the selling price is $3.50, the cost mark-up can be solved in the following ways:

cost mark-up = selling price ÷ portion cost

= $14.00 ÷ $4.80

= 2.9166

= 2.92

or cost mark-up = 1 ÷ food cost percentage

= 1 ÷ 34.285%

= 1 ÷ 0.34285

= 2.91674

= 2.92

The cost mark-up can be used to determine a selling price when a portion cost is known by multiplying the cost mark-up and the portion cost:

Example 32: Determine a selling price

selling price = portion cost × cost mark-up

For example, if the ingredients for a portion of soup costs $1.05 and the restaurant has a cost mark-up of 3.6, the menu price of the soup is:

selling price = portion cost × cost mark-up

= $1.05 × 3.6

= $3.78

The restaurant would charge at least $3.78 for the menu item if it wants to keep its mark-up margin at 3.6, which is about a 28% food cost percentage. This price might be adjusted because of competition selling the same item for a different price, price rounding policies of the restaurant or the whims of management. For example, many restaurants have prices that end in 5 or 9 (such as $4.99 or $5.95). Prices on such menus tend to be rounded to the nearest number ending in 5 or 9. No matter what the final menu price is, at least a base price has been established.

The problem with the above approach is it doesn’t explain how to select a food percentage or a selling price from which to derive the percentage. In many cases, the food percentage is based on past experiences of the manager, or by a supposed awareness of industry averages. For example, many people simply set their food percentage at 30% and never work out a more appropriate figure. Similarly, the selling price of a menu item is often the product of guessing what the market will bear: $4.50 for a bowl of soup may seem like a good deal or as much as a reasonable person might pay in that restaurant. Unfortunately, none of these methods takes into account the unique situations affecting most restaurants.

A more accurate way of computing a target food cost percentage is to estimate total sales, labour costs, and hoped-for profits. These figures are used to determine allowed food costs. The total of projected food costs is divided by the projected sales to produce a food cost percentage. The food cost percentage can be turned into a mark-up margin by dividing the percentage into 1, as shown above.

Example 33

For example, to determine the food cost percentage of a restaurant that has projected sales of $10 000 and labour costs of $6000, overhead of $1000, and a goal of before-tax profits of $500, the following procedure is used:

food costs = sales − (labour costs + overhead + profit)

= $10 000 − ($6000 + $1000 + $500)

= $10 000 − ($7500)

= $2500

food percentage = food costs ÷ sales

= $2500 ÷ $10 000

= 0.25

= 25%

mark-up margin = 1 ÷ food percentage

= 1 ÷ 25%

= 1 ÷ 0.25

= 4

In this example, the menu prices would be determined by multiplying the portion costs of each item by the mark-up margin of 4. Adjustments would then be made to better fit the prices to local market conditions.

If the application of the derived mark-up margin produces unreasonable prices, then one or more of the projected sales, labour costs, overhead, or profits are probably unreasonable. The advantage of using this system is that it points out (but does not pinpoint) such problem assumptions early in the process.

A similar approach uses a worksheet as shown in Figure 21.

In the middle section of the worksheet in Figure 21, a food cost percentage is determined by subtracting other known cost percentages (i.e., operating costs, labour cost, and profit wanted) from 100%. One divided by the food cost percentage determines the mark-up margin. Food costs are then determined in the bottom half of the sheet and a menu price derived by multiplying the total cost by the mark-up margin.

In this pricing method, a “profit wanted” percentage is added to the cost of each menu item. This builds some potential profit into the menu prices. If you were to price everything according to costs only, the restaurant would only ever be able to break even and never turn a profit.

Contribution Margins

On the surface, it seems that the lower the food cost, the more room there is for profit. In one sense this is true, as the percentage profit is obviously greater for an item that has a food cost percentage of 25% (or 75% percentage profit) than an item that has a food percentage cost of 45% (or 55% percentage profit). However, in terms of monetary profit, the issue is not that straightforward. What has to be determined is how much money the menu item generates. This calculation involves finding the contribution margin of each item.

Example 34: Contribution margin

Contribution margin is determined by subtracting the cost from the selling price. An item that costs $2.00 to make and sells for $3.00 has a contribution margin of:

contribution margin = selling price − cost price

= $3.00 − $2.00

= $1.00

Consider the contribution margin of two menu items that have different food costs and food cost percentages shown in Figure 22.

Figure 22: Contribution margin

| Item | Food Cost | Selling Price | Food Cost % | Contribution Margin |

|---|---|---|---|---|

| Chicken | $4.50 | $16.50 | 27% | $12.00 |

| Steak | $9.00 | $24.00 | 38% | $15.00 |

In terms of percentage profit, the chicken is higher. However, in terms of money in the till, the steak creates more money that can be used to pay bills. The key to a good menu is not necessarily to just keep food cost percentages low; it is to also to keep contribution margins high.

Balancing the Menu to Achieve Targets

Menu Analysis

A basic menu analysis determines how often each item on the menu is sold. This basic statistic can be used with cost percentages, menu prices, and sales values to make generalizations about the relative value of each menu item. Figure 23 shows a menu analysis worksheet for a lunch menu. Most POS systems can generate this type of information at the end of a shift, day, week, or month.

Figure 23: Menu analysis worksheet

| A | B | C | D | E | F | G | H | I | J |

| Menu Item | Total Sold | Menu Price | Portion Cost | Food Cost % | Portion C.M.[1] | Total Food Sales | Total Food Cost | Total C.M. | C.M.% |

|---|---|---|---|---|---|---|---|---|---|

| Hamburger | 12 | $10.95 | $2.75 | 25% | $8.20 | $131.40 | $33.00 | $98.40 | 24% |

| Cheeseburger | 8 | $11.95 | $4.25 | 36% | $7.70 | $95.60 | $34.00 | $61.60 | 15% |

| BLT sandwich | 10 | $11.95 | $3.75 | 31% | $8.20 | $119.50 | 37.50 | $82.00 | 20% |

| Ham sandwich | 5 | $10.95 | $3.50 | 32% | $7.45 | $54.75 | 17.50 | $37.25 | 9% |

| Fried chicken | 4 | $14.95 | $5.25 | 35% | $9.70 | $59.80 | $21.00 | $38.80 | 9% |

| Clubhouse | 6 | $12.95 | $4.00 | 31% | $8.95 | $77.70 | $24.00 | $53.70 | 13% |

| Steak sandwich | 5 | $15.95 | $7.25 | 45% | $8.70 | $79.75 | 36.25 | $43.50 | 10% |

| Totals | 50 | $618.50 | $203.25 | $415.25 |

The statistics provided in a menu analysis have several uses. For example, the total sold statistics can be used to predict what future sales numbers will be. This information is valuable for ordering supplies and organizing the kitchen and kitchen staff to produce the predicted number of items.

Even more important than popularity is the contribution margin of each item. Often an average contribution margin is found and compared with the contribution margin of individual items.

Example 35: Average contribution margin

The average contribution margin in the example above is found by dividing the total contribution margin (total of Column I) by the number of sales (total of Column B):

average margin = total margin ÷ number of sales

= $415.25 ÷ 50

= $8.31

The contribution margin for each item is found by subtracting the cost of the item from the selling price. In the example in Figure 23, the contribution margins are given in Column F.

Some decisions can be made comparing items:

- The hamburgers, cheeseburgers, BLTs, and ham sandwiches are below the average contribution margin. The first three items are good sellers and account for over half of the sales (30/50 = 60%) and they may be able to pull their weight by slightly increasing their prices. By adding $0.50 to the menu price of each of these items, they would each have a contribution margin above or close to $8.31.

- The ham sandwich is significantly lower than the average margin and is also low in sales. It might be best to drop this item from the menu and replace it with something else.

- The fried chicken has a good contribution margin but its sales are a little on the low side. To increase sales, the chicken might be given more prominence on the menu or might be offered as part of a special with a small salad for a slight increase in price. As long as the additions have a reasonable food cost percentage and are inexpensive compared to the portion cost of the chicken, the increase in sales should have a positive impact on the total contribution margin (the values in Column I).

The type of menu analysis must be tempered with common sense. Because averages are used to determine an acceptable margin or level of sales, some menu items will automatically be under the average just as some will have to be above the average. If items that are under the average are replaced, the next time a menu analysis is done there will be a new average and other items under that average. Taken logically, your menu options will run out before you have every item being exactly at the average!

Given that menu items are usually broken down into categories, this type of analysis is most effective when comparing similar items. An analysis of all of the desserts or starters to compare their margins is much more effective than comparing the margin of a dessert against a lobster dinner, which by the very nature of its price and cost will always have a higher contribution margin.

Profitability

You want to sell menu items that have a high margin of profitability. The relative profitability of an item is calculated by comparing its contribution margin to the average contribution margin (ACM) of all items. The contribution margin is the selling price of a menu item minus the standard food cost of the item. This is the amount that the item contributes to the labour cost, other costs of doing business, and profit. The ACM equals the total contribution margin divided by total numbers of items sold. Profitable items have a contribution margin equal to or higher than the ACM.

Desserts and appetizers may have lower contribution margins than entrées. This is because these items generally have lower prices and cannot contribute the same dollar value of contribution margin, even though their food cost percentage may be lower than entrée items. Also, the restaurant may wish to tempt patrons to add these items to their purchase, increasing the average cheque size. If you can sell more to an individual guest, you increase the revenues without increasing the labour costs and other costs to the same extent.

For example, if the customer orders and appetizer before the entrée, he or she does not take up any more time in the restaurant (that is, the customer does not decrease seat turnover) because the appetizer is served and eaten during the normal waiting time for preparing the main dish. As well, the additional labour of the server is minimal because even without ordering an appetizer service may still be needed to provide additional bread or refill water glasses. Thus, the sale of the appetizer will increase the profitability of the restaurant even though the contribution margin is not as high.

Desserts may also have a low contribution margin. Often desserts are purchased ready-made (e.g., cakes and cheesecakes). There may be little labour cost in serving these items so the overall contribution of the dessert item to profitability is high.

Items that require little preparation (that is, have a low labour cost) may still generate a significant contribution to margin even when their food costs are higher. Even if the food cost of the item was very high and the CM low, you would want to keep this item because the combined labour cost and food cost is low. Thus the amount this item contributes to the fixed cost of the business is high.

Potential Profitability of Menu Items

To determine the potential profit in a menu item, you must have a good idea of the potential cost of producing the item. Pre-costing the menu means you determine the cost of producing every item on the menu under ideal conditions. The assumption is that cooks will follow directions, the portions will be accurately measured, and all the portions will be sold. The results are the optimum costs; in reality costs could be higher.

Popularity

Another factor to consider when reviewing your menus is the popularity of an item. Popularity is determined by comparing sales of items to expected popularity. The expected popularity is the predicted menu mix (sometimes called the sales mix) if each of the menu items in a category were equally popular.

An example is provided in Figure 24, which lists seven appetizers. The expected popularity would be 100% divided by 7 (the number of menu items) or 14.3%. Menu analysis assumes that popular items have sales of 70% or more of the expected popularity. In the example, appetizers would have to exceed 10% (70% of 14.3%) of appetizer sales in order to be considered popular. Which of the items are popular?

Figure 24: Menu analysis worksheet

| Menu Item | Total Sold | Menu Price | Portion Cost | Food Cost % | Portion C.M. | Total Food Cost | Total Food Sales | Total C.M. | C.M.% |

|---|---|---|---|---|---|---|---|---|---|

| Thai Wings | 31 | $6.75 | $1.93 | 28.59% | $4.82 | $59.83 | $209.25 | $149.42 | 4.63% |

| Dry Ribs | 211 | $6.75 | $1.72 | 25.48% | $5.03 | $362.92 | $1,424.25 | $1,061.33 | 31.54% |

| Nachos | 71 | $6.95 | $1.53 | 22.01% | $5.43 | $108.63 | $493.45 | $384.82 | 10.61% |

| Calamari | 19 | $7.50 | $2.23 | 29.73% | $5.27 | $42.37 | $142.50 | $100.13 | 2.84% |

| Soup and Salad | 78 | $5.95 | $1.55 | 26.05% | $4.40 | $120.90 | $464.10 | $343.20 | 11.66% |

| Thai Salad | 129 | $6.45 | $1.68 | 26.05% | $4.77 | $216.72 | $832.05 | $615.33 | 19.28% |

| Cajun Caesar | 130 | $6.95 | $1.76 | 25.32% | $5.19 | $228.80 | $903.50 | $674.70 | 19.43% |

| Total Appetizer | 669 | ACM = | $4.98 | $1,140.70 | $4,469.10 | $3,328.93 | 100.00% |

You can see at a glance that Dry Ribs is the most popular appetizer, followed by Thai Salad and Cajun Caesar. Nachos and Soup & Salad fall just slightly over the 10% boundary. Thai Wings and Calamari show dismal results in terms of popularity with only 4.63% and 2.84% of appetizer sales.

Sales of menu items are analyzed to put menu items in four categories:

- Popular and profitable

- Popular but not profitable

- Not popular but profitable

- Neither popular nor profitable

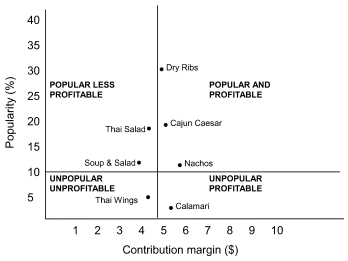

Figure 25 displays graphs the popularity of the appetizers from the example over these four categories. The graph shows popularity on the vertical axis and contribution margin on the horizontal axis. A line is drawn vertically to indicate the ACM and horizontally to show 70% of expected popularity. This allows you to see at a glance which category an item falls into: A) Less popular and profitable, B) popular and profitable, C) unpopular and unprofitable, and D) Unpopular and profitable.

The graph shows that Thai Wings and Calamari were very unpopular menu items, but it also provides information on profitability. Thai Wings has a contribution margin that is lower than the ACM for appetizers. Calamari has a contribution margin that is higher than the ACM.

Computer programs may automatically calculate contribution margins and popularity. The information may be presented in tables or spreadsheets as shown above, or in a four-box analysis, with less detail, as shown in Figure 26.

Figure 26: Four-box analysis of appetizer items

| Unprofitable | Profitable | |

|---|---|---|

| Popular | Thai Salad, Soup and Salad | Dry Ribs, Cajun Caesar, Nachos |

| Unpopular | Thai Wings | Calamari |

Menu Revisions

Popular and profitable items are ones you want to maintain on your menu. Maintain the specifications of the item rigidly. Do not change the quality of the product served. Feature the item in a prominent location on the menu. You want to sell this item, so make sure that customers see it. Have servers suggestively sell the item. For example, when asked for suggestions, they could say, “You may want to try our Linguine Chicken. It is very popular. It has a cream sauce with lots of fresh basil.” Test the possibility of increasing prices by raising the price slightly.

If an item is popular but not profitable, you want to see if you can increase the contribution margin without reducing its popularity. Increase prices carefully and gradually. If the item is attractive because of its high value, it may still be a good value after a price increase. You could also increase the contribution margin by reducing the cost of the accompaniments. For example, you might substitute less costly vegetables. You might also try to reduce costs by decreasing the portion size. If you are unable to improve the item’s popularity, you may want to relocate it to a lower profile part of menu. If the item has a very low labour cost, you may be able to justify the lower contribution margin because less revenue is needed to compensate for the labour cost.

Not popular but profitable items are often a puzzle. You want to sell these items, but your challenge is to encourage the guests to buy them. Shift demand to these items by repositioning them on the menu. Encourage servers to suggestively sell these items. Consider decreasing the price slightly or adding value by offering a larger portion size, more expensive accompaniments or garnishes. However, you need to be cautious so that you do not change the item into a popular but unprofitable item.

Items that are neither popular nor profitable are obvious candidates to remove from the menu. They are not pulling their weight. The only time such an item might be left on the menu is if it provides an opportunity to use leftovers and has low labour costs associated with its preparation.

Using Specials and Feature Items

Another way to balance the menu is by using daily specials and feature items. For example, assume you have been tracking your food costs using a daily food cost control sheet (refer back to Figure 20). It is halfway through the month and you are running a slightly higher than average food cost for the month so far. Choosing to run specials that have lower food costs or having the staff feature and promote the better food cost items should help to bring the targets in line by the end of the month.

Arranging Items on the Menu

Another way of engineering the menu is by strategically arranging the items on the menu. Some menus use callout or feature boxes to highlight certain items, others have pictures featuring certain menu items, and others may note an item as a house specialty. These are all ways to attract the attention of the customer, and in most cases, you will find that it is these items that sell the best. If these items also have high contribution margins and/or low food costs, they will increase profitability. Featuring the items with the lowest margins and highest food costs will have the opposite effect, and likely mean that you will not be in business for very long.

There are also some psychological reasons that things will sell on a menu. Often the most expensive or the least expensive item will not sell as well as other items on the menu because customers do not wanting to appear either extravagant or cheap in front of their guests. Using descriptions that entice the customer (e.g., “award-winning,” “best in the city”) will increase the sale of a particular item, but make sure you can deliver on the promise!

All in all, balancing the menu is something that takes time and experience to do well, but is a skill that you will need to run a profitable kitchen.

- C.M. = Contribution margin ↵

1. To maximize profitability by encouraging customers to buy what you want them to buy

2. Structuring of a menu to balance low- and high-profit items to achieve overall target food costs and profit

Portion of sales that can be applied against fixed costs; gross sales minus variable costs.

The amount of profit a business generates compared to sales, usually reflected in a percentage.